Introduction: The New Tax Era and Its Impact on Retirement Planning

The landscape of U.S. tax policy has experienced a dramatic transformation with the enactment of the One Big Beautiful Bill Act in 2025. This new law permanently extends the Tax Cuts and Jobs Act tax brackets, creating a stable, long-term environment that significantly alters retirement planning strategies. For many retirees and aging populations, this change has turned Roth IRA conversions from a short-term maneuver into a key, long-range strategy to manage longevity risk and increase the potential for tax-free growth.

In this opinion editorial, we take a closer look at the evolving tax environment and explore the opportunities presented by Roth IRA conversions. We will discuss tax diversification, estate planning benefits, and the need to carefully figure a path through potential tax pitfalls. Using tables, lists, and detailed explanations, we guide you through the twists and turns of this new tax reality.

Assessing the New Tax Landscape After the OBBBA Act

Before 2025, the looming expiration of the low federal tax rates under the Tax Cuts and Jobs Act (TCJA) created a sense of urgency among retirees. The impending shift was expected to push retirees into higher tax brackets once the temporary provisions expired in 2026. However, the passage of the One Big Beautiful Bill Act has permanently locked these rates, ranging from 10% to 37% with inflation-adjusted thresholds, thereby removing a critical time pressure.

This legislative change provides retirees with the flexibility to plan their Roth IRA conversions over several years rather than feeling forced into a rapid decision-making process. With permanently low rates, the environment encourages a measured approach that can help manage tax liability more effectively over time. As a result, many advisors now recommend seeing Roth IRA conversions as a critical component of a long-term retirement strategy, where thoughtful planning can lead to significant tax-free growth for future income needs.

Understanding the Stability: Permanent TCJA Tax Brackets

One of the essential features of the new tax law is the permanence of TCJA tax brackets. This stability means that retirees can now “fill up” their lower tax brackets incrementally, converting portions of their pre-tax traditional IRA into Roth IRAs without the fear of sudden tax hikes. Consider a married couple filing jointly with $150,000 in taxable income in 2025 who can, for instance, convert up to $56,700 of their savings without spilling into a higher tax bracket. This opportunity to strategize conversions over multiple years is a key advantage in today’s tax planning climate.

Such stability not only fosters better tax planning but also allows retirees to address the tricky parts of navigating high cumulative tax burdens later in life. As a result, managing your tax profile becomes less nerve-racking and more a matter of assembling a balanced retirement income portfolio.

Opportunity for Roth IRA Conversions Amid a Stable Low-Rate Future

With the new legislative framework, Roth IRA conversions have emerged as an attractive option to secure long-term tax benefits. The ability to convert traditional IRAs to Roth accounts without the conventional rush has profound implications for retirees. This shift is especially important as it transforms these conversions into a core retirement strategy designed to counteract the risk of outliving one’s savings.

Why Convert Now? Strategic Advantages of a Steady Tax Environment

Previously, many retirees viewed Roth conversions as a temporary measure to capitalize on the temporarily low tax rates. Now, with these rates set in stone, the process has morphed into a continuous strategy to enjoy tax-free growth over a prolonged period. The forced withdrawal requirements imposed on traditional IRAs, starting at age 73 under the Secure Act 2.0, can notably disrupt retirement income without thoughtful planning. In contrast, Roth IRA accounts do not impose required minimum distributions (RMDs) during the account holder’s lifetime, thereby preserving capital and allowing the funds to grow undisturbed.

This stability not only offers key flexibility in planning but also serves as a foundation for crafting a diversified tax strategy. By gradually converting sizeable portions of retirement savings into Roth IRAs, individuals can mitigate the overall tax burden, ensuring that they secure lower tax liabilities for years to come. In this regard, ongoing strategic planning is super important to take full advantage of the current low-rate environment.

Understanding Longevity Risk and Tax-Free Retirement Solutions

One of the primary concerns for individuals approaching retirement is the risk of outliving their available funds, a scenario known as longevity risk. As people live longer, they face the increased possibility of depleting their savings, which makes it critical to establish a retirement income plan that offers both stability and growth over many decades.

Combating Longevity Risk with Roth IRA Benefits

Roth IRAs provide a dual solution in this context. Firstly, they allow tax-free growth and withdrawals, meaning that the money continues to compound without being trimmed away by taxes. Secondly, since there are no mandatory withdrawals during the account holder’s lifetime, the funds can continue to grow unhindered. These features effectively counter the forced sale of assets that often accelerates portfolio depletion when traditional IRAs are involved.

For many retirees, the strategy of converting funds to Roth IRAs has become a critical maneuver—a way to build a more robust, secure income stream that is less vulnerable to the complications associated with sudden changes in tax policy. By strategically converting assets over time, retirees can address the long-term risk of outliving their savings, ensuring that they maintain a financial cushion that protects against uncertain future expenses.

Tax Diversification: Crafting a Flexible Income Strategy for the Future

Tax diversification remains a key component of a resilient retirement plan. In an unpredictable tax policy environment, having a balance between pre-tax and tax-free retirement accounts can be the cornerstone for adaptive income planning. With Roth IRA conversions, retirees gain an adjustable tool for managing their overall tax liability both now and in the future.

Building a Balanced Portfolio: Pre-Tax vs. Tax-Free Accounts

This strategy allows retirees to “feel around” for the best way to minimize tax burdens when withdrawing funds. The idea is to steer through the tax system by carefully deciding when to pull from tax-deferred accounts versus tax-free accounts. Here are some of the benefits of tax diversification:

- Flexibility: By having both types of accounts, retirees can adjust withdrawals based on current tax environments.

- Risk Management: If future tax rates rise, drawing from Roth IRAs ensures a tax-free income stream; if tax rates fall, pre-tax accounts can be utilized more efficiently.

- Long-Term Planning: Tax diversification offers a robust framework for managing the financial complications associated with longevity.

The deliberate mix of these two income sources helps in managing the small distinctions between varying income levels. It imparts a sense of comfort that, regardless of how tax policies evolve, retirees have the means to work through puzzling tax issues in a way that minimizes unexpected burdens.

Estate Planning and Protection Against the “Widow Tax”

Another compelling rationale for opting for Roth IRA conversions is the estate planning advantage they offer. Retirement savings often serve as a crucial component of one’s legacy, providing a financial foundation for heirs. The new tax environment also presents unique benefits for surviving spouses who might otherwise face increased tax rates when transferring assets.

Tax-Free Inheritance: A Legacy Without Burdens

Roth IRAs are especially attractive in estate planning due to their tax-free nature when inherited. Under current regulations, beneficiaries are granted up to a 10-year window to withdraw funds, allowing the assets to grow tax-free during this period. This benefit can be vital in compounding wealth for future generations without eroding the principal with taxes.

For surviving spouses, the risk of encountering the “widow tax”—a term used to describe the spike in tax rates that can occur when moving from a Married Filing Jointly status to a Single filer status—can be quite intimidating. Roth IRA income, being tax-free, provides a cushion against this often-overlooked complication, ensuring that financial support remains consistent during a vulnerable time.

Estate Planning Strategies: Key Considerations

When devising an estate plan that leverages Roth conversions, retired individuals should consider the following elements:

- Timing of Conversions: Align the conversion timeline with broader estate planning goals, ensuring that future generations can benefit maximally.

- Tax-Free Growth: Maximize the funds available for heirs by allowing the account to benefit from tax-free compounding for as long as possible.

- Protection Against Rate Increases: Lock in the current low federal rates, thereby mitigating the risk associated with potential future tax hikes that could affect traditional IRAs.

In many respects, these benefits underscore the essential need to plan ahead, balancing both current financial needs and long-term legacy goals in a comprehensive manner.

Identifying Hidden Tax Traps: Understanding IRMAA, NIIT, and SALT Limitations

While the advantages of Roth IRA conversions are significant, retirees must be mindful of several hidden tax pitfalls that can complicate an otherwise solid strategy. With larger conversions, there are potential issues that can inadvertently inflate one’s tax liability throughout retirement.

Understanding Potential Tax Pitfalls

When converting pre-tax assets to Roth IRAs, the increase in modified adjusted gross income (MAGI) can lead to unintended consequences. Some of these issues include:

- IRMAA Surcharges: Medicare’s Income-Related Monthly Adjustment Amount is sensitive to income levels. A large conversion can trigger expensive surcharges.

- Net Investment Income Tax (NIIT): This additional tax on investment income can be triggered by a higher MAGI, increasing the overall tax burden.

- SALT Cap Considerations: High state and local tax (SALT) deductions are phased out at certain income levels, potentially reducing deductible expenses.

Assessing the Impact in High-Tax States

For retirees residing in states with high tax rates—like California—the combined federal and state effective tax rates can soar to 45% or even 50%. The compounded effect of IRMAA, NIIT, and the limitations of SALT deductions can result in a nerve-racking tax scenario. To help illustrate this, consider the following table, which outlines some of the key impacts of these hidden costs:

| Tax Item | Trigger Point | Potential Impact |

|---|---|---|

| IRMAA Surcharge | Increased MAGI due to large conversions | Additional monthly premiums for Medicare |

| NIIT | MAGI above threshold levels | Additional 3.8% tax on investment income |

| SALT Cap | High state and local tax payments | Limits on deductible tax amounts |

Given these factors, it is critical that retirees work with knowledgeable advisors to figure a path through these hidden problems. Even the most attractive opportunity can be riddled with tension if the subtle parts of tax policy are overlooked.

Strategic Execution: Timing and Funding Roth Conversions

One of the most critical elements of a successful Roth conversion strategy is timing. Retirees must carefully choose when to convert their pre-tax assets to ensure that they remain within favorable tax brackets. This is especially true in years when income levels are lower—such as shortly after retirement, during a market downturn, or in any situation where taxable income temporarily dips.

Practical Tips for Timing Conversions

Here are several practical strategies to keep in mind when planning your Roth conversions:

- Convert During Lower Income Years: Opt for years when your taxable income is relatively low to minimize the impact on your tax bracket.

- Monitor Market Conditions: During market downturns, account values might be lower, allowing you to convert assets at a reduced cost.

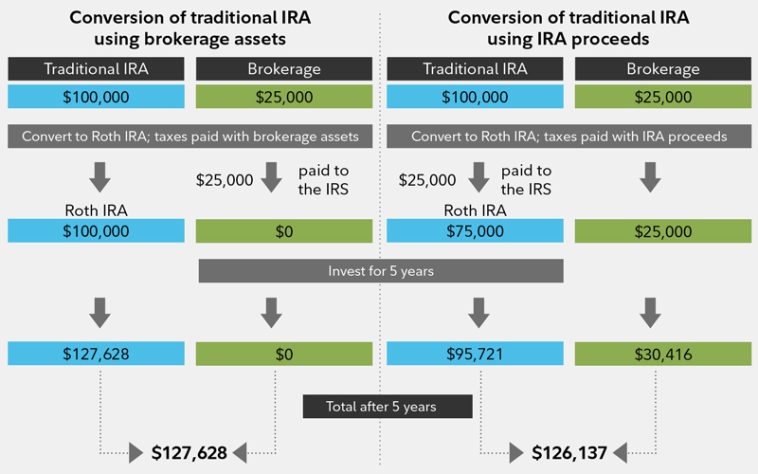

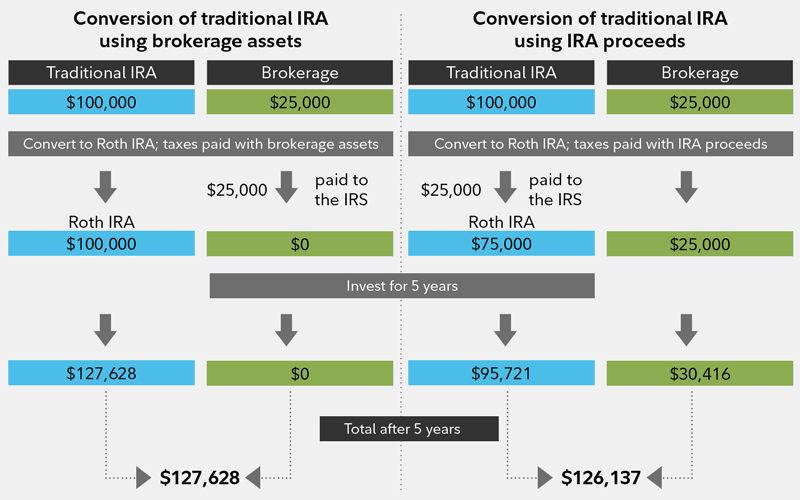

- Avoid Using Retirement Funds to Pay Taxes: Whenever possible, pay the conversion tax from non-retirement accounts such as taxable brokerage accounts. This approach maximizes the amount that gets converted and left to compound tax-free in your Roth IRA.

Funding Strategies: A Comparative Look

When considering how to fund the taxes associated with a Roth conversion, it is important to compare the benefits of using different sources. Below is a simplified comparison:

| Funding Source | Advantage | Disadvantage |

|---|---|---|

| Taxable Brokerage Account | Maintains full principal in the IRA for tax-free growth | May require liquidating other investments |

| Retirement Account Funds | Simple and direct source of cash | Reduces the amount converted, lowering long-term compounding potential |

Such careful planning ensures that the conversion process is not only effective in the immediate term but also contributes to long-lasting tax benefits. The key is to manage your conversions with finesse, taking into account not just current conditions but also future uncertainties.

Preparing for Future Uncertainties: Roth Conversions as a Hedge

Even with the permanent low tax brackets brought about by the new legislation, the realities of fiscal policy remain unpredictable. The national debt, which now hovers around $36.60 trillion, looms large as a reminder that future tax increases could be imminent. In this context, Roth IRA conversions can serve as an effective hedge against rising tax rates, offering protection when conventional wisdom might otherwise falter.

Hedging Against the Uncertain Future

Locking in today’s low tax rates through gradual Roth conversions is a strategic move that can protect retirees against possible future tax hikes. By converting portions of your retirement assets at predictable and relatively low tax rates, you are effectively safeguarding your portfolio against the unpredictable twists and turns of future tax policy. In many respects, this thoughtful approach not only provides present flexibility but also builds a more resilient retirement income stream.

Moreover, this approach offers an added benefit: it provides a dual form of security, allowing retirees to simultaneously plan for longevity while also preparing for potential shifts in tax policy. It represents a holistic way to consider both aging and fiscal uncertainty concurrently.

Policy, Perspective, and the Future of Tax Reform

While many critics might voice concerns that the permanence of these low tax brackets could lead to complacency, it is important to take a balanced view of policy and perspective. The new tax laws, like any legislation, are not without their tricky parts and subtle details that require careful attention. However, they also offer a level of predictability that many retirees have not experienced in decades.

Looking Ahead: What Does the Future Hold?

In looking forward, it is essential to remain vigilant about potential changes while also embracing the opportunities that the current legislation offers. Tax policy is a moving target, and prudent retirement planning must be able to adjust as needed. Retirees should continue to work with seasoned advisors who can help them steer through the tangled issues of tax planning, ensuring that their strategies remain robust as economic and fiscal conditions evolve.

As we observe the continuing evolution of tax policy, one thing remains clear: strategic planning and proactive management will always be super important. The current era of permanent low tax brackets offers a rare window of predictability that, if exploited wisely, can significantly enhance the quality of retirement life.

Conclusion: A Proactive Approach in a Tax-Efficient Retirement Strategy

The legislative evolution marked by the One Big Beautiful Bill Act 2025 has ushered in a new era for retirement planning in the United States. By permanently extending the low federal tax brackets, the law offers retirees a tremendous opportunity to reframe Roth IRA conversions as a long-term, flexible strategy for addressing longevity risk, ensuring tax-free growth, and safeguarding their estates against future uncertainties.

While there are still challenging bits to be managed—such as avoiding the unexpected triggers of IRMAA surcharges, NIIT, and high state taxes—the benefits of a well-executed Roth conversion strategy are clear. Retirees have an unprecedented chance to assemble a diversified portfolio that balances pre-tax and tax-free assets, providing a robust hedge against both longevity risk and potential future tax increases.

This opinion editorial encourages those planning for retirement to take a closer look at Roth IRA conversions as more than just a financial maneuver; it is a comprehensive approach that addresses multiple facets of retirement income planning. By taking your time, converting gradually during lower-income years, and always being mindful of the hidden tax traps, you set the stage for a retirement that is not only sustainable but also resilient in the face of fiscal challenges.

Working through these decisions with a trusted, qualified financial advisor is super important. Together, you can devise a strategy that considers all the subtle details—from the tax-free growth benefits of Roth accounts to the long-term estate planning advantages they provide. It is this balanced, forward-thinking approach that will help ensure that retirees and their heirs thrive in an era that is both promising and unpredictably full of twists and turns.

As the tax policy landscape continues to adapt to economic and fiscal pressures, taking a proactive approach today by converting to Roth IRAs could be the cornerstone of a more secure, tax-efficient future. In the complex world of retirement planning, anchoring your strategies in stability and forward-thinking tax planning provides a clear and steady path through the maze of potential pitfalls, ensuring that financial security remains both achievable and enduring.

In summary, the permanence of the TCJA tax brackets as established by the OBBBA Act represents a turning point in retirement planning. It converts the once short-term tactic of Roth IRA conversions into a long-term strategy that helps mitigate the risks of longevity, infuse flexibility into income planning, and shield future generations from unexpected tax burdens. The time has come to reconsider how you approach your retirement plan, making the most of a system that now rewards patience, strategic planning, and thoughtful execution.

Your journey through this new tax era may be filled with its own set of tricky parts and tangled issues, but with careful attention to planning—even as you work your way through hidden tax traps—the rewards can be significant. Embrace the opportunity to convert steadily, invest wisely, and plan comprehensively. In doing so, you are not only protecting your financial future but also laying a stronger foundation for the legacy you leave behind.

Ultimately, the decisions you make today about Roth conversions are about more than just immediate tax savings; they are a critical piece in building a resilient retirement income strategy that can withstand the unpredictable challenges of tomorrow. With thoughtful planning and a clear understanding of the current tax environment, harnessing the benefits of Roth IRA conversions could well be the smartest move for ensuring long-term financial freedom and success.

Originally Post From https://www.ainvest.com/news/roth-ira-conversions-post-gop-tax-law-era-strategic-planning-longevity-tax-efficiency-2508/

Read more about this topic at

Focused conversion: A strategy for IRAs

3 Strategies for Reducing Roth Conversion Taxes